Building an Emergency Fund for Moms: Free Emergency Fund Calculator

Building an emergency fund is a crucial step in securing your family’s financial future. For moms, having a robust emergency fund can provide peace of mind and financial stability during unexpected situations. Knowing that you have money saved for emergencies provides immense peace of mind. As a mom, you have enough to worry about; having an emergency fund means one less thing to stress over.

This blog post is all about building an emergency fund for moms.

Understanding Emergency Funds

An emergency fund is a cash reserve for unplanned expenses or financial emergencies. Having an emergency fund can help you avoid debt and financial stress. An emergency fund provides a financial buffer that can keep you afloat in a time of need without relying on credit cards or high-interest loans. It’s essential to have a cash reserve for unexpected expenses or financial emergencies.

Why Moms Need an Emergency Fund

What does financial stability mean to you?

For me, financial stability means having a reliable and consistent flow of income that covers all household expenses, including bills, groceries, healthcare, and childcare, without stress or uncertainty. It also involves having a sufficient emergency fund to handle unexpected expenses, such as medical emergencies or sudden car repairs, and the ability to save for future goals, like children’s education or family vacations.

Financial stability ensures that moms can provide for their family’s needs while also planning for long-term financial security, reducing the stress and anxiety of economic uncertainty. I aim to save money to cover 9-12 months of all my living expenses if I lose my job or experience another emergency that prevents me from earning money for my family.

Unexpected Expenses

Life is full of surprises, many of which come with a hefty price tag. From car repairs to sudden school expenses for your kids, unexpected costs can quickly derail your budget. If you are a homeowner, you know how these expenses can derail you from your financial goals or put you back into debt.

Within the last three years, I’ve had to pay for septic tank cleaning, roof repair (where insurance refused to pay), and new HVAC. I paid it all with credit cards because I had insufficient money for these emergencies. The interest charges alone set me back several years in my debt-free journey. That is why I started building my emergency funds in a High Yield Savings account.

Avoiding debt and financial instability

Learn from my mistakes and avoid debt and financial instability by starting your emergency savings fund. Without an emergency fund, you may rely on credit cards or loans, making debt harder to pay off. It took me several years to pay off the HVAC and Septic tank repairs!

Determining Your Emergency Fund Goal

Let me start by saying there are no hard rules for building an emergency fund. You do what makes you feel secure and financially stable. However, if you do not know where to start, here are a few guidelines to follow.

How to Calculate Your Emergency Fund

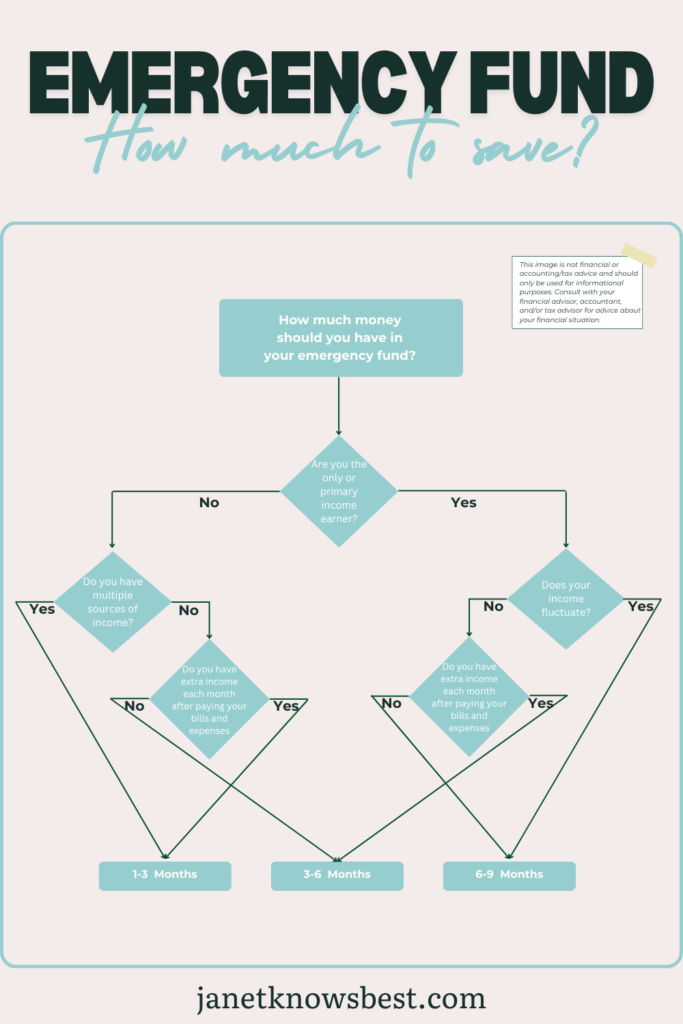

The typical goal for an emergency fund is to cover three to six months’ expenses. Factors like job security, industry stability, household size, income, expenses, and marital status should determine the size of your emergency fund. For those nearing retirement, the size of your emergency fund may vary depending on your circumstances.

Emergency Fund Calculator

If you need help determining how much money you need in your emergency fund and how long you should save, here is my FREE Emergency Fund Calculator.

You can use this free emergency fund calculator to determine how much money you need to save and for how long you should be saving. I also provide a decision tree to help you decide when to spend the emergency funds.

Choosing the Right Savings Account

If you keep your money in the bank rather than stuffing it in a cash envelope, keep your emergency savings in a separate account, not in your checking or other savings goals. I personally keep my emergency fund in a high-yield savings account. It is a good place for your money, as it is federally insured for up to $250,000 per depositor, per ownership category, and per financial institution.

You should compare top savings accounts to find a high-yield savings account with a great rate. This way, you can earn interest as you build an emergency fund! A high-yield savings account can provide a safe and accessible place to store your emergency fund.

Building Your Emergency Fund

I personally set up direct deposit into my high-yield savings account. You can also set up automatic monthly transfers from your checking account to your savings account. This can help you build an emergency fund by ensuring you are prioritizing this goal in your budget.

You should also consider using tax refunds, bonuses, or raises to boost your emergency fund. I get a bonus every March, and I always set aside money to help me fund my savings goals faster. That is how I funded my initial $1000 this year.

Overcoming Savings Obstacles

Saving money can feel like a daunting task, especially when you’re juggling debt and dealing with irregular income or expenses. However, with a strategic approach and some practical tips, you can overcome these obstacles and build a solid financial foundation.

Paying off debt while building your emergency fund

Start with a $1000

When you have debt, the first step is to build a $1000 Emergency Fund. This fund acts as a financial safety net, allowing you to handle unexpected expenses without using credit cards or loans. To create this fund:

- Calculate Your Monthly Expenses: Determine how much you spend each month on essentials like rent, utilities, groceries, and transportation.

- Set Up a Separate Savings Account: Open a dedicated savings account to keep your emergency fund separate from your regular checking account.

- Automate Your Savings: Set up automatic transfers to your emergency fund account. This will make saving effortless and consistent.

After you’ve saved $1000, your target should be to save for one month’s worth of expenses, then two, then three, and so on.

Dealing with irregular income or expenses

Irregular income or expenses can complicate budgeting, but with the right tools and strategies, you can stay on top of your finances.

Use a Budgeting App or Budget Planner

Budgeting apps can be incredibly helpful in tracking your spending and managing irregular income.

They allow you to:

- Track Expenses in Real Time: Link your bank accounts and credit cards to track your spending automatically.

- Set Spending Limits: Establish spending limits for different categories and receive alerts when approaching or exceeding these limits.

- Analyze Spending Patterns: Gain insights into your spending habits and identify areas for improvement.

If you are an app gal, then you can try the following popular budget apps:

- YNAB, for hands-on zero-based budgeting

- EveryDollar, for simple zero-based budgeting

- PocketGuard, for a simplified budgeting snapshot

- Honeydue, for budgeting with a partner

- Goodbudget, for hands-on envelope budgeting

If you are a pen-to-paper gal, I recommend the Budget By Paycheck Workbook by the Budget Mom.

If you are a Google sheet or Excel gal, I recommend the Press Reset Ultimate Wealth Dashboards.

Using Your Emergency Fund Wisely

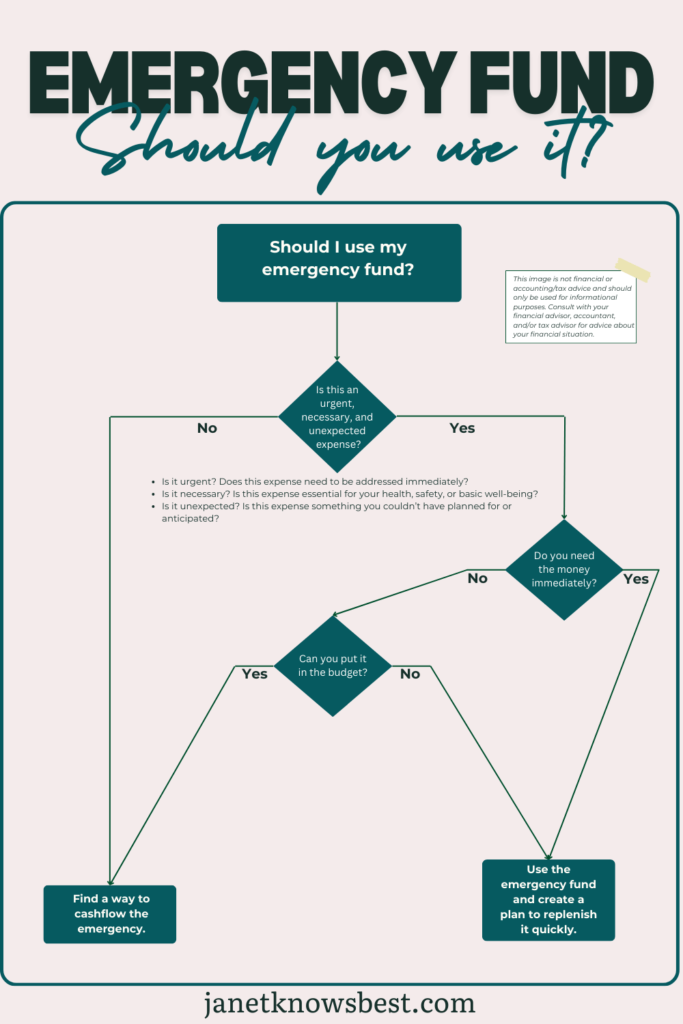

Your emergency fund is your financial safety net, designed to help you navigate unexpected challenges without derailing your long-term financial goals. To make the most of this crucial resource, it’s important to use it wisely. And yes, this means you cannot use it for last-minute gifts, eating out, or shopping for the latest deals.

Identifying True Emergencies

Your emergency fund should be reserved for genuine emergencies—urgent, necessary, and unexpected situations. Common examples include (from real-life personal experience):

- Medical Bills (OBGYN): Unexpected medical expenses can arise from sudden illness, injury, or emergency procedures not covered by insurance.

- Septic Tank or Plumbing Repairs: If your toilet backs up, you will find a way to pay for this expense.

- Home Repairs: Urgent repairs, such as a leaking roof or first-floor flooding, that threaten your safety or home’s integrity qualify as emergencies.

Avoiding Non-Essential Expenses

Establish guidelines for an emergency or unplanned expense to avoid dipping into your emergency fund for non-essential expenses. Ask yourself the following questions before using your fund:

- Is it urgent? Does this expense need to be addressed immediately?

- Is it necessary? Is this expense essential for your health, safety, or basic well-being?

- Is it unexpected? Is this expense something you couldn’t have planned for or anticipated?

Consistency is key to maintaining the integrity of your emergency fund. Avoid using it for discretionary spending such as vacations, gifts, or entertainment. These expenses should be planned separately and within your budget.

Maintaining and Growing Your Emergency Fund

Your financial situation and needs can change, so regularly reviewing and adjusting your emergency fund goal is important. Consider the following steps:

- Assess Your Expenses: Periodically re-evaluate your monthly expenses and adjust your emergency fund target accordingly.

- Increase Your Goal Over Time: As your income grows or your responsibilities increase, aim to boost your emergency fund to cover a longer period of expenses.

Achieving Financial Peace of Mind

Achieving financial peace of mind is especially important for moms, as it provides both security and flexibility to handle unexpected challenges. To start building your emergency fund, set a clear goal and explore ways to make it a reality. This might include cutting non-essential expenses, automating savings, or finding additional sources of income. By taking these steps, you can ensure that you are well-prepared for any financial surprises and enjoy greater peace of mind, knowing that you and your family are financially secure.

This blog post was all about emergency funds for moms.