11 Best Ways To Save Money For Kids – The Ultimate Guide

As a mom, my greatest desire is to provide a better future for my children than the one I had. I want to give them the opportunities and resources I never had. For me, this means finding ways to save money for my kids’ future so they do not have to endure the same financial struggles that I went through. My parents, despite their best intentions, were never able to save for my future because they were struggling to make ends meet.

I refuse to let history repeat itself. I am committed to breaking the cycle of poverty and ensuring that my children have a secure and stable financial foundation to build upon. My determination to save for my kids’ future stems from the hardships I faced growing up and the belief that they deserve better. I want to give them every advantage possible so that they can thrive and succeed in life.

This blog post is all about the best ways to save money for kids in 2024-2025.

There are various ways you can begin saving money for your children. I recommend that you read about each method and do your own research to determine which method is best for you.

- Make sure you are financially stable first.

- Open a UGMA or UTMA Account.

- Open a Certificate of Deposit (CD) Account.

- Open a Coverdell Education Savings Account (ESA).

- Explore An Achieving a Better Life Experience Account (ABLE).

- Leverage a 529 college savings or prepaid tuition plan.

- Use a Roth IRA.

- Set aside money in a Trust Fund.

- Open a High Yield Savings Account (HYSA).

- Open a Health Savings Account (HSA).

- Use Savings Bonds.

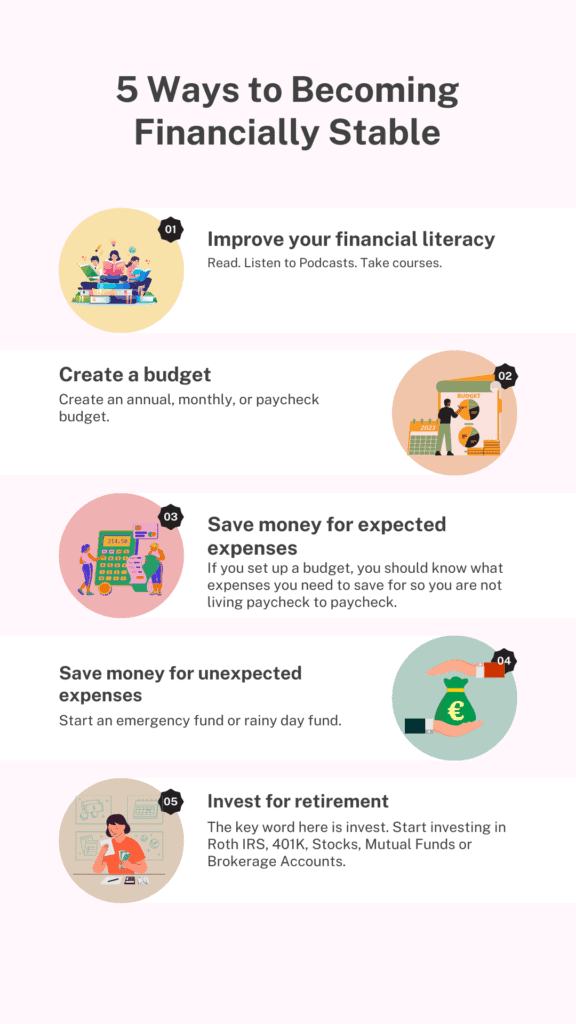

Make sure you are financially stable first.

The best way to save money for your kids is to work on your own personal finances and learn good money habits to set a positive example for them. Demonstrating responsible financial behaviors, such as budgeting, saving, and investing wisely, can help create a stable financial foundation for your family’s future. Teaching your children about the value of money and the benefits of saving early on can empower them to make sound financial decisions throughout their lives.

Recommended Actions:

- Improve your financial literacy.

- Create a budget. Check out the free annual budget template.

- Have an emergency fund.

- Save money for expected expenses.

- Open a high yield savings account.

- Open investment accounts.

- Invest for retirement.

I know it is easier said than done, but you have to start saving and investing for yourself before you can start saving for your kids. For me, the first step is to get out of debt. I started my debt-free journey to pay over 300K+ of debt, including student loans, my mortgage, and consumer debt. I am also saving my emergency fund in a high-yield savings account and savings for retirement in my 401K retirement account.

Check out my YouTube channel, where I document my financial success journey.

Open a Custodial Account.

A great way to save money for kids is through custodial accounts. Custodial accounts are accounts set up for minors, usually by their parents or guardians, to save and invest money on their behalf. The adult manages the account and decides how the money is used until the child reaches a certain age, usually 18 or 21.

Custodial accounts allow parents to save for their child’s future early on. The money in the account can be used for things like education expenses, home purchases, or other important milestones in the child’s life. Additionally, custodial accounts can help teach kids about financial responsibility and the importance of saving and investing. Let’s explore all the different types of custodial accounts.

Open a UGMA or UTMA Account

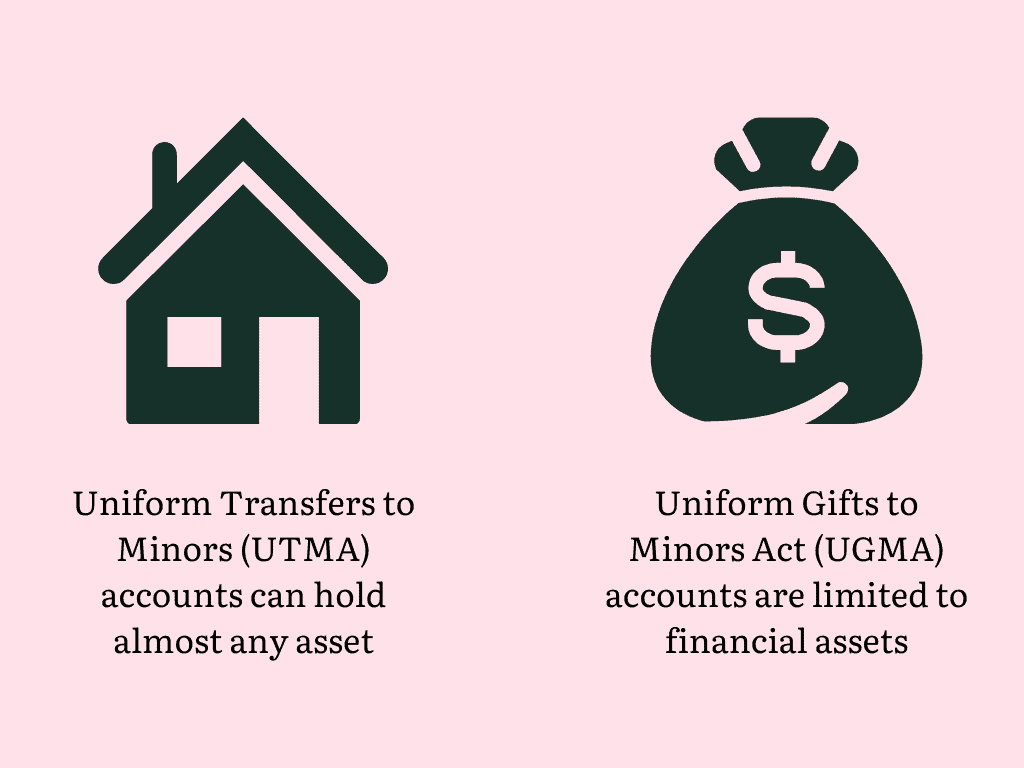

UTMA (Uniform Transfers to Minors Act) and UGMA (Uniform Gifts to Minors Act) accounts are taxable custodial accounts established for the benefit of a minor. These accounts allow a parent or guardian to make financial gifts or transfers to a minor without establishing a trust.

The UGMA Act allows gifts of cash or securities to be given to minors without tax implications. The UTMA Act expanded gifts to include property and other transfers for those states that have adopted it. Once the minor reaches the age of majority, they gain full control over the account and are free to use the assets as they see fit.

The main difference between UGMA and UTMA accounts is that UGMA accounts involve irrevocable gifts to the minor, while UTMA accounts provide more flexibility as the assets can be withdrawn by the custodian.

UGMA or UTMA Contribution Limits (Deposit Limits)

You can make contributions with after-tax dollars. According to IRS rules, you can contribute up to $18,000 annually without incurring a gift tax in 2024 ($36,000 per married couple). The first $1,250 of any earnings from a custodial account may be exempt from federal income tax. The IRS taxes the next $1,250 at the child’s tax rate, also called the “kiddie tax.” Anything over that is subject to income tax at the parent’s tax rate.

What are Qualified Expenses for a UGMA or UTMA Account?

UGMA and UTMA accounts provide more flexibility in how the funds can be used compared to a 529 plan. While you’ll need to use the funds in a 529 plan for specific educational expenses to avoid a penalty, you can use funds in a UGMA/UTMA account for anything that benefits the child.

However, it is important to consider the potential impact on financial aid eligibility and tax implications when setting up these accounts. You don’t receive a tax deduction for adding money to UTMA and UGMA accounts. Instead, you just reduce the taxes on investment gains. When it comes time to FAFSA and student aid, UGMA and UTMA accounts are reported as a child’s asset, reducing financial aid eligibility.

Pros and Cons of a UGMA or UTMA Account

PROS

CONS

Open a Certificate of Deposit (CD) Account

A CD account, or a certificate of deposit account, is a type of savings account offered by banks, credit unions, or brokerages. When you open a CD account, you deposit a certain amount of money into it. This money is typically not meant to be touched for a set period of time, which can range from a few months to several years.

CD Contribution Limits (Deposit Limits)

There are generally no limits, but FDIC insures only up to $250,000. To invest in a CD on behalf of a dependent, parents and guardians must open a custodial account, such as a UGMA or UTMA account. This means the same rules apply: You cannot change the beneficiary of the account once you’ve opened it, earnings from $1,250 – $2,500 will be taxed at the child’s rate, and earnings above $2,500 will be taxed at the parent’s rate.

What are Qualified Distributions for a CD Account?

In exchange for keeping your money in the CD for the agreed-upon time period, the bank pays you interest. The interest rate is usually fixed, meaning it stays the same throughout the CD’s term. If you do withdraw the money before the term is up, you may face penalties, such as losing some of the interest you’ve earned.

Pros and Cons of a Deposit (CD) Account

PROS

CONS

Open a Coverdell Education Savings Account (ESA)

A Coverdell Education Savings Account, or ESA, is a trust account created by the U.S. government to help families pay their children’s or guardians’ educational expenses. Your child or guardian must be under 18 when the account is established. The age restriction may be waived for special needs cases.

ESA Contribution Limits (Deposit Limits)

While more than one ESA can be set up for a single beneficiary, the total maximum contribution per year for any single kid is $2,000.

What are Qualified Expenses for an ESA?

When the contributions are distributed, they are tax-free if used for qualified education expenses, including tuition, books, equipment, special needs services, and even academic tutoring. ESA account funds can also be used for primary and secondary schools (K–12 grades).

These accounts are comparable to the 529 tax-free college savings plan. However, unlike a 529, when your child turns 30, any remaining funds in the ESA must be disbursed.

Pros and Cons of a Coverdell Education Savings Account (ESA)

PROS

CONS

Explore An Achieving a Better Life Experience Account (ABLE)

An Achieving a Better Life Experience account or ABLE is a tax-advantaged savings account to which contributions can be made to meet the qualified disability expenses of the owner, or designated beneficiary. Funds from these 529A ABLE accounts can help designated beneficiaries pay for qualified disability expenses. Distributions are tax-free if used for qualified disability expenses.

ABLE Contribution Limits (Deposit Limits)

An eligible individual may have only one ABLE account. Any person may contribute to an ABLE account for an eligible beneficiary. Typically, contributions for an ABLE account may not exceed the annual gift tax exemption ($18,000 in 2024).

However, if the beneficiary is working, and they or their employer are not making certain retirement plan contributions, the beneficiary may contribute an additional amount equal to the lesser of their annual compensation or the individual Federal Poverty Level for a one-person household in their state of residence for the prior calendar year.

What are Qualified Expenses for ABLE?

You can take distributions from your ABLE account to pay for any qualified disability expenses, such as expenses for maintaining or improving your health, independence, or quality of life. Qualified disability expenses include those for education, housing, transportation, employment training and support, assistive technology, personal support services, health, prevention and wellness, financial management, administrative services, legal fees, expenses for oversight and monitoring, and funeral and burial expenses.

Pros and Cons of ABLE Accounts

PROS

CONS

Leverage a 529 college savings or prepaid tuition plan.

One of the best ways to save for kids is to open a 529 plan for your child’s future educational expenses, such as college tuition or college costs. Money in this custodial account can grow tax-deferred, and if the withdrawals are used for qualifying education expenses, the withdrawals are tax-free.

The money you put into your 529 plan isn’t just sitting there doing nothing. It gets invested in things like stocks, bonds, or mutual funds. This means your money can grow over time, hopefully earning more than just sitting in a regular savings account.

529 Plan Contribution Limits (Deposit Limits)

In 2024, the IRS allows individuals to contribute up to $18,000 per beneficiary per year to a 529 plan without affecting their lifetime gift tax exemption. For married couples filing jointly, the limit is $36,000.

What are Qualified Expenses for a 529 Plan?

Qualified expenses include required tuition and fees, books, supplies and equipment including computer or peripheral equipment, computer software and internet access and related services if used primarily by the student enrolled at an eligible education institution. Someone who is at least a half-time student, room and board may also qualify.

- Student Loan Repayment – Student loan repayment is now a qualified expense on the federal level, but it may not be eligible in your state. You can take out $10,000 per individual as a lifetime limit. See our section below on this new feature. Read our full guide to using a 529 plan for student loan repayment here.

The Setting Every Community Up for Retirement Enhancement Act of 2019 [P.L. 116-94], also known as the SECURE Act, changed the definition of qualified distributions from a 529 plan to allow 529 plans to be used to repay the principal and/or interest on qualified education loans of the beneficiary and the beneficiary’s siblings. Refer to The College Investor to learn more.

- K-12 Tuition – Tuition at a public or private K-12 school is a qualified expense on the federal level up to $10,000 per year, but it may not be eligible in your state. Refer to The College Investor to see if your state qualifies.

- IRA Rollover – Starting in 2024, you can potentially roll over up to $35,000 into a Roth IRA. However, this is a limited option with many restrictions, and some states may not allow this. Refer to The College Investor to learn more.

These plans, named after Section 529 of the Internal Revenue Code, are sponsored by states, state agencies, or educational institutions and are authorized by Congress. There are two main types of 529 plans:

- College Savings Plans: These function like a 401(k) or IRA but are specifically tailored for education expenses. Contributions to these plans are invested in mutual funds or similar investment vehicles. The value of the plan can fluctuate based on the performance of the chosen investments.

- Prepaid Tuition Plans: These allow tuition prepayment at participating colleges and universities. They can help lock in current tuition rates, protecting against future tuition inflation. However, prepaid tuition plans typically only cover tuition and fees, not other expenses like room and board.

Each state may offer its own 529 plan with different features, investment options, and tax benefits within these two types. Some states also offer tax deductions or credits for contributions to their 529 plans. It’s essential to research and compare the features of different plans to find the one that best suits your needs and financial goals.

Pros and Cons of a 529 college savings or prepaid tuition plan

PROS

CONS

Check out 529 Plans: The Ultimate Guide To College Savings Plans

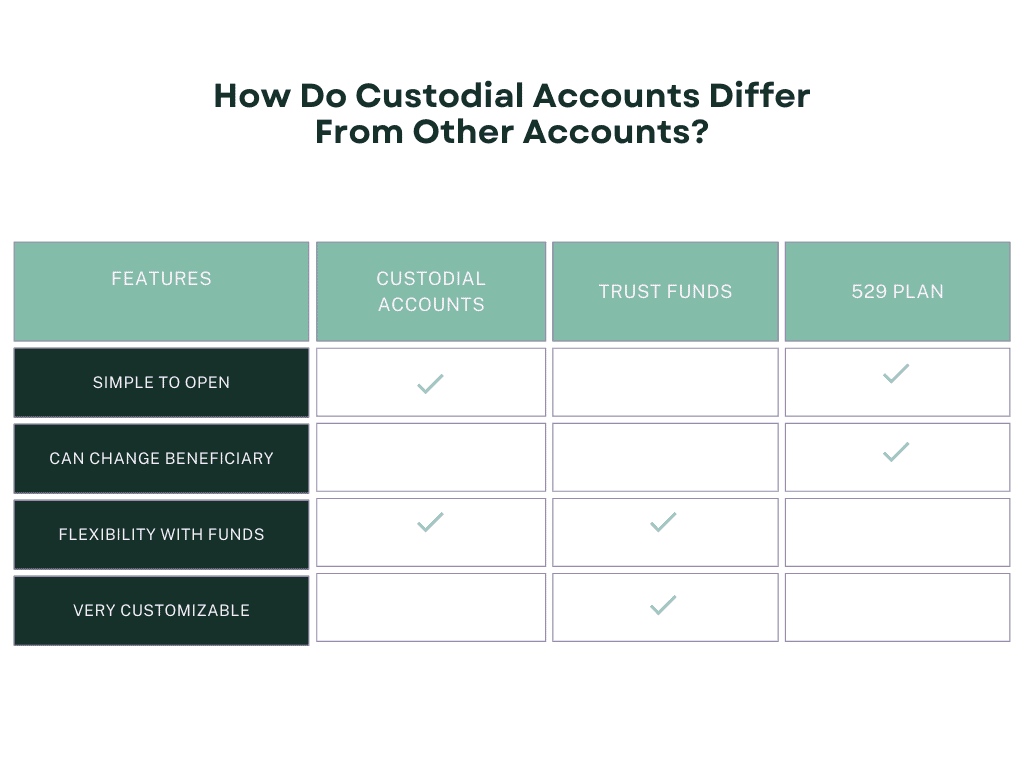

UTMA or UGMA vs. 529 Vs. Coverdell ESA

If you saving for you kids education is a key goal for you and your family then it is good to understand these accounts and how they compare.

According to IRS rules, both 529s and Coverdell ESAs are meant to be used for qualified educational expenses, otherwise withdrawals are subject to a 10% federal penalty. UTMA and UGMA accounts do not have the same requirements (qualified educational expenses) when it comes to withdrawals.

529s and Coverdell ESAs are are also subject to contribution limits. There are no annual contribution limits for 529s, but there are aggregate contribution limits that you need to consider. ESAs have annual contribution limits and eligibility restrictions based on income. UTMA and UGMA accounts do not have any limitations on contributions.

However, 529s and Coverdell ESAs provide tax-advantaged benefits whereas UTMA and UGMA contributions are taxable accounts. With 529s, the beneficiary can be changed to another if the current beneficiary doesn’t need the money, which is not possible with UTMA and UGMA accounts.

Use a Custodial Roth IRA.

A custodial Roth IRA is a tax-advantaged retirement account that is owned by a minor, but controlled by an adult custodian until the minor reaches legal adulthood. There’s no age limit. Even babies can contribute to a Roth IRA. However, to open a custodial Roth IRA, the minor needs to be earning an income (either through an employer or entrepreneurial jobs like babysitting, cutting grass or tutoring).

Custodial Roth IRA Contribution Limits (Deposit Limits)

In 2024, the contribution limit is $7,000, or $8,000 if you’re 50-plus. The Roth IRA income limits are $161,000 for single tax filer and $240,000 for those married filing jointly.

What Are Qualified Distributions for Roth IRAs?

A qualified distribution is any payment or distribution from your Roth IRA that meets the following requirements.

- It is made after the 5-year period beginning with the first tax year for which a contribution was made to a Roth IRA set up for your benefit.

- The payment or distribution is:

- Made on or after the date you reach age 59½,

- Made because you are disabled (defined earlier),

- Made to a beneficiary or to your estate after your death, or

- One that meets the requirements listed under First home under Exceptions in chapter 1 (up to a $10,000 lifetime limit).

- Made on or after the date you reach age 59½,

If you receive a distribution from your Roth IRA that isn’t a qualified distribution, part of it may be taxable. However, you may not have to pay the 10% additional tax in the following situations.

- You have reached age 59½.

- You are totally and permanently disabled.

- You have been certified as having a terminal illness.

- You are the beneficiary of a deceased IRA owner.

- You use the distribution to buy, build, or rebuild a first home.

- The distributions are part of a series of substantially equal payments.

- You have unreimbursed medical expenses that are more than 7.5% of your AGI (defined earlier) for the year.

- You are paying medical insurance premiums during a period of unemployment.

- The distribution is a corrective distribution.

- The distributions are for your qualified higher education expenses.

- The distribution is due to an IRS levy of the IRA or retirement plan.

- The distribution is a qualified reservist distribution.

- The distribution is a qualified birth or adoption distribution.

- The distribution is a qualified disaster distribution or qualified disaster recovery distribution.

Pros and Cons of a Custodial Roth IRA

PROS

CONS

Set aside money in a Trust Fund.

A trust fund is a fund held in a trust by a trustee (organization or person who administers the trust). It is a legal entity that holds property or assets for the benefit of another (the beneficiary). People often think of trust funds as something rich parents create for their kids, but they’re not just for the wealthy.

Trusts help regular folks too, by making sure their stuff goes to the right people after they die, without a lot of legal fuss. Trust funds can hold assets like money, houses, or stocks. A trustee, who’s like a manager, takes care of the trust and makes sure things go where they’re supposed to, to benefit the person the trust is for.

Irrevocable Trust vs. Revocable Trust

There are several types of trust funds which fall into two main categories.

- Irrevocable Trust: This is a type of trust in which the terms of the trust become permanent. You cannot change them, even if you are funding the trust. This is also why these trusts are completely protected.

- Revocable Trust or Living Trust: This is a type of trust that you can retain control over but it will also remain subject to seizure by creditors and other parties.

If you decide to create a trust fund for your kids, please contact a legal and financial professional. Trusts can become very complicated and tricky to navigate.

Pros and Cons of a Trust Fund

PROS

CONS

Open a High Yield Savings Account (HYSA).

I recently opened my first high yield savings account to build my emergency fund. However, I decided to open a 529 Account to save for my son’s future. I am also planning to open another high yield savings account to make automatic transfers to grow my savings for unexpected living expenses. I also recently found that kids can get a head start with a high yield savings account as well.

What is a High Yield Savings Account?

A high-yield savings account is a type of savings account that typically offers a higher interest rate than traditional or regular savings accounts. These accounts are offered by online banks and some traditional banks as well. The higher interest rate allows you to earn more on your savings compared to a standard savings account.

As mentioned above, the main benefit of a HYSA is that it offers higher rates. According to the Federal Deposit Insurance Corporation (FDIC), a regular savings account’s national average interest rate is just 0.46% (as of 4/15/24). Plenty of banks and credit unions offer savings accounts for minors, though the law requires a parent or guardian to open and jointly own the accounts.

With several kids’ savings accounts on the market, the best options aren’t always easy to spot. Here are some factors to consider when shopping for a savings account for your child.

What are the Benefits of a Kids Savings Account?

Opening a savings account for your child or teenager comes with various advantages. Firstly, having their own account can be a practical way to educate them on managing money. Kids who have their own bank accounts tend to develop positive financial behaviors, such as saving consistently and avoiding impulsive spending.

A kids’ savings account also offers a platform for setting and working towards future goals. Whether saving for their education, a first car, or a desired gadget, children can learn the value of saving for desired items. Introducing a savings account to your child instills a sense of independence and responsibility from an early age.

Pros and Cons of a High Yield Savings Account (HYSA)

PROS

CONS

Open a Health Savings Account (HSA).

A Health Savings Account (HSA) is a tax-advantaged savings account used in conjunction with a high-deductible health plan (HDHP) to cover eligible medical expenses. Both individuals and employers can contribute pre-tax dollars to an HSA, and the funds can be used to pay for qualified medical expenses such as medical bills, doctor visits, prescription medications, and certain medical procedures.

I personally have an HDHP and an HSA for myself and my family. It is the best option for us because of the tax advantages and the ability to save for future healthcare expenses. My employer also contributes to this account, so it is “free money” that I would miss out on. I am currently using this money to pay for my son’s medical bills and my pregnancy medical expenses.

A Health Savings Account can be a valuable tool for parents looking to save for medical expenses and take advantage of tax benefits. However, before opening an HSA, it’s important to weigh the potential drawbacks, such as higher out-of-pocket costs and contribution limits.

Pros and Cons of a Health Savings Account (HSA)

PROS

CONS

Use Savings Bonds.

Savings bonds are a type of investment vehicle issued by the U.S. Department of the Treasury that can be purchased by individuals as a way to save money and earn a return on their investment over time. They are considered low-risk investments because they are backed by the full faith and credit of the U.S. government.

Savings bonds are typically purchased at a discount to their face value and accrue interest over a set period of time, usually ranging from 20 to 30 years. Once they reach their maturity date, they can be redeemed for their full face value plus any accrued interest.

There are two main types of savings bonds: Series EE bonds and Series I bonds.

- Series EE bonds earn a fixed interest rate and earn interest plus a guaranteed return of double the value if kept for 20 years.

- Series I bonds earn a combination of a fixed rate and an inflation-adjusted rate calculated twice a year.

Savings bonds can be used for various purposes, such as education expenses, retirement savings, or as a general savings vehicle for your kids’ future expenses. Savings bonds can be a valuable addition to a diversified investment portfolio, providing a safe and secure way to save money for your kids’ future.

I have not purchased savings bonds because I prioritize paying off debt and contributing to a 401 (K) and a 529 Fund. However, I will definitely consider purchasing these in the near future, as they are a reliable option for those looking for a low-risk investment vehicle.

Pros and Cons of Savings Bonds

PROS

CONS

Conclusions

As a newish mom, I want to do everything in my power to ensure my kids have options in the future and are set up to go to college if they wish to do so. I also want to instill financial independence and good money behaviors early in their lives.

And in the first step is to increase my own financial literacy and develop good money habits so I can lead by example. I do highly suggest that you reach out to a financial or legal professional before making in decisions that can impact your family.

I hope you enjoyed this blog post which was all about ways to save money for kids – your kids!